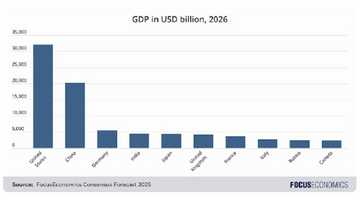

Global economic forecasts for 2026 show that the United States is expected to remain the world’s largest economy, with an estimated gross domestic product of $32.1 trillion, according to projections from Focus Economics.

America continues to dominate in areas such as artificial intelligence, finance, healthcare, aerospace, and advanced manufacturing, helping it maintain a significant lead over other nations.

Rapid innovation in Silicon Valley, strong consumer spending, and the influence of global financial markets have all contributed to the country’s economic strength.

Source: UGC

According to Focus Economics’ forecast, of the top 10 largest economies in 2026, five will be in Europe, three in Asia and two in the Americas.

1. United States — $32.1 trillion

The United States is projected to stay at the top of the global economic rankings, contributing more than a quarter of worldwide nominal GDP. Its economy is highly diversified, with major strengths in technology, healthcare, defense, entertainment, and financial services.

Read also

Nigeria’s SEC announces date for transition to T+1 settlement cycle

Companies based in Silicon Valley continue to lead advancements in artificial intelligence, cloud computing, and biotechnology, while Wall Street remains the center of global finance.

The U.S. also benefits from a strong consumer market, high productivity, and ongoing investments in clean energy and semiconductor production.

2. China — $20.2 trillion

China is expected to remain the world’s second-largest economy, powered by its enormous manufacturing sector and export capacity. The country dominates global production in electronics, machinery, batteries, and textiles, while also expanding rapidly in electric vehicles and renewable energy technology.

Despite its industrial strength, China faces growing economic pressures from a declining birth rate, rising debt, and challenges in the property market. Even so, its massive domestic market and infrastructure network continue to make it a major force in global trade.

3. Germany — $5.4 trillion

Germany continues to hold its position as Europe’s largest economy, supported by a strong industrial and export-oriented foundation.

Read also

Petrol depot prices rise as MRS, AP, other filling stations adjust rates

The country is globally recognized for its automotive, engineering, and chemical industries, with brands like BMW, Mercedes-Benz, and Siemens contributing heavily to economic output. Germany’s “Mittelstand” — thousands of medium-sized manufacturing firms — remains central to its success.

The country is also investing heavily in green technology and energy transition projects following recent energy supply disruptions in Europe.

4. India — $4.5 trillion

India is projected to become one of the fastest-growing major economies in the world. Growth is being fueled by information technology, digital services, manufacturing, and rising consumer demand.

A large and youthful population has helped expand the labor force and domestic market, while government initiatives focused on infrastructure, digital payments, and local manufacturing continue to attract foreign investment. India’s growing startup ecosystem and leadership in software outsourcing are also strengthening its global economic influence.

5. Japan — $4.4 trillion

Japan remains one of the world’s leading industrial economies, known for its expertise in robotics, automobiles, precision engineering, and electronics. Companies such as Toyota, Sony, and Panasonic continue to shape global markets.

However, Japan faces long-term economic challenges due to an aging population, low birth rates, and slower domestic consumption. Even with these obstacles, the country remains a technological leader with strong export capabilities and advanced infrastructure.

Read also

Top 10 most affordable states to live in Nigeria in 2026 as food prices rise

6. United Kingdom — $4.2 trillion

The United Kingdom continues to rank among the world’s largest economies, driven mainly by its service sector. London remains one of the leading global financial centers, with banking, insurance, legal services, and real estate playing major roles in the economy.

The UK also has strong industries in pharmaceuticals, education, creative media, and technology. Although the country continues adjusting to post-Brexit economic realities, it remains a major destination for global investment and international business.

7. France — $3.6 trillion

France maintains a highly diversified economy with strengths in luxury goods, tourism, agriculture, aerospace, and energy. Global corporations such as Airbus and LVMH continue to boost the country’s international economic profile.

France is also one of the world’s most visited tourist destinations, which contributes significantly to national income. In recent years, the government has increased investments in renewable energy, innovation, and digital transformation to strengthen long-term competitiveness.

Source: UGC

8. Italy — $2.7 trillion

Read also

CBN releases fresh exchange rates as naira falls, Access, UBA, Zenith other banks price dollar high

Italy’s economy combines a strong service sector with globally recognized manufacturing industries. The country is especially known for fashion, luxury goods, machinery, food production, and automobile manufacturing.

Northern Italy remains the industrial heart of the economy, home to many export-driven businesses and family-owned enterprises. Tourism also plays a crucial role, with millions of visitors contributing to sectors such as hospitality, transportation, and retail each year.

9. Russia — $2.5 trillion

Russia’s economy continues to rely heavily on oil, natural gas, and other natural resources. Energy exports remain the country’s main source of government revenue and foreign exchange earnings.

Despite facing international sanctions and geopolitical tensions, Russia has continued trading with several Asian and Middle Eastern markets. The country also maintains significant industries in defense, mining, and agriculture, though long-term growth remains uncertain due to external economic pressures and limited foreign investment.

10. Canada — $2.4 trillion

Canada rounds out the top 10 largest economies, supported by abundant natural resources and a stable financial system. The country is a major exporter of oil, natural gas, timber, minerals, and agricultural products.

Read also

Dangote Refinery to sell shares via POS, Opay, Moniepoint as Nigerians prepare for historic IPO

In addition to its resource industries, Canada has strong banking, technology, and service sectors concentrated in cities such as Toronto, Vancouver, and Montreal. Immigration and trade partnerships with the United States continue to play important roles in supporting economic growth.

Economists believe the global economy in the coming years will be shaped by several key forces, including advances in technology, demographic shifts, climate and energy policies, supply chain changes, and geopolitical tensions. These factors are expected to influence not only economic growth rates but also the balance of power among the world’s largest economies in the future.

Top 10 most corrupt countries in the world

Meanwhile, Legit.ng earlier reported that South Sudan and Somalia are the most corrupt countries globally, according to the 2025 Corruption Perceptions Index (CPI).

This is according to the report released by Transparency International on Tuesday, February 9, 2026, after assessing 182 countries worldwide

Libya, Eritrea, and Sudan are other African countries in the top ten most corrupt countries in the world.

Source: Legit.ng